Does Australia have a current account surplus? (Yes -- and it's kind of a big deal)

The quick version:

Australia has a current account surplus (CAS)

This is the first time Australia has recorded a CAS since the late 1970s

Australia’s CAS is caused by its Balance on Goods and Services surplus. The Net Primary Income balance is still in deficit.

Australia has a current account surplus. This is important

When I studied Economics at high school we never talked about a current account surplus (the CAS). Australia simply didn’t record a CAS. Instead, Australia was known for its current account deficits (CAD).

Things have changed in 2022. Australia has had a CAS for a period of time and it’s an economic statistic that signals some important things about the Australian economy.

Let’s rewind a little.

My HSC Economics exam and writing about a current account deficit

When I sat my HSC Economics exam, we only ever wrote about Australia having a current account deficit. We NEVER talked about current account surpluses.

Have a look at this stimulus for one of the essay questions.

Source: NESA

You can see that the current account balance for 1997/98 was a deficit for $23 billion. Let’s fast forward to now.

In the September quarter of 2021, Australia recorded a CAS of nearly $22 billion.

This CAS shrank to around $13 billion in the December quarter. But Australia still has a current account surplus.

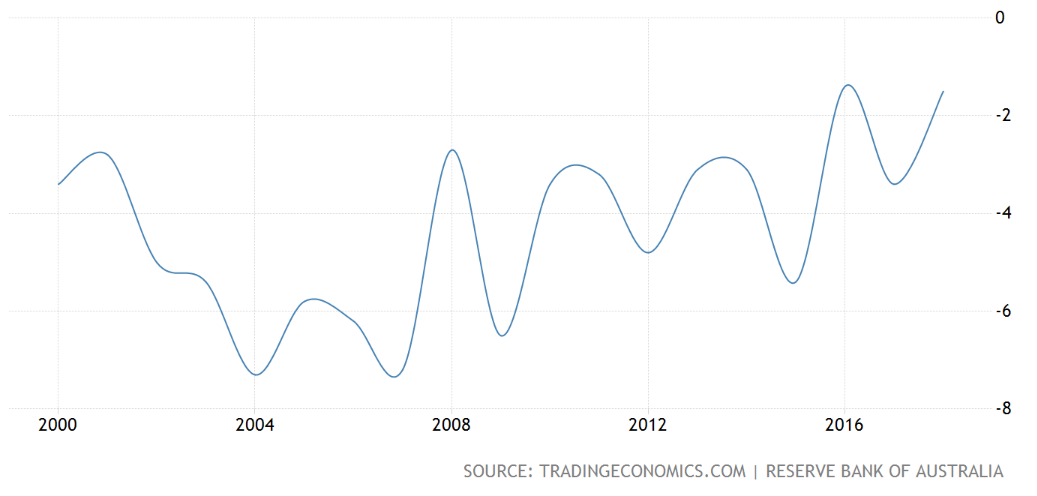

On a personal note, I never thought Australia would have a CAS. Why would I? Have a look at this graph below. For my lifetime (up until now), Australia has had a persistent CAD.

The numbers on the right hand side of the graph represent the size of the current account balance as a percentage of GDP. So the larger the % of GDP, the larger the size of the CAD. You can see that in the mid-2000s the CAD was over 7% of GDP – a very large amount.

Why does Australia have a current account surplus in 2022?

The key drivers of Australia’s CA balance are:

The Balance on Goods and Services (BoGS)

The Net Primary Income (NPY) balance

As the value of BoGS and NPY change, so does the balance on the current account. Typically, Australia’s BoGS fluctuates considerably – due to the frequent changes in the prices and volumes of our exports. For example, the price of iron ore rarely stays the same. It’s not like manufactured goods that have relatively consistent prices. An iPhone’s price doesn’t fluctuate from day to day.

Australia has a persistent NPY deficit. This hasn’t changed.

So why has the CA has moved into surplus? Because of Australia’s BoGS surplus.

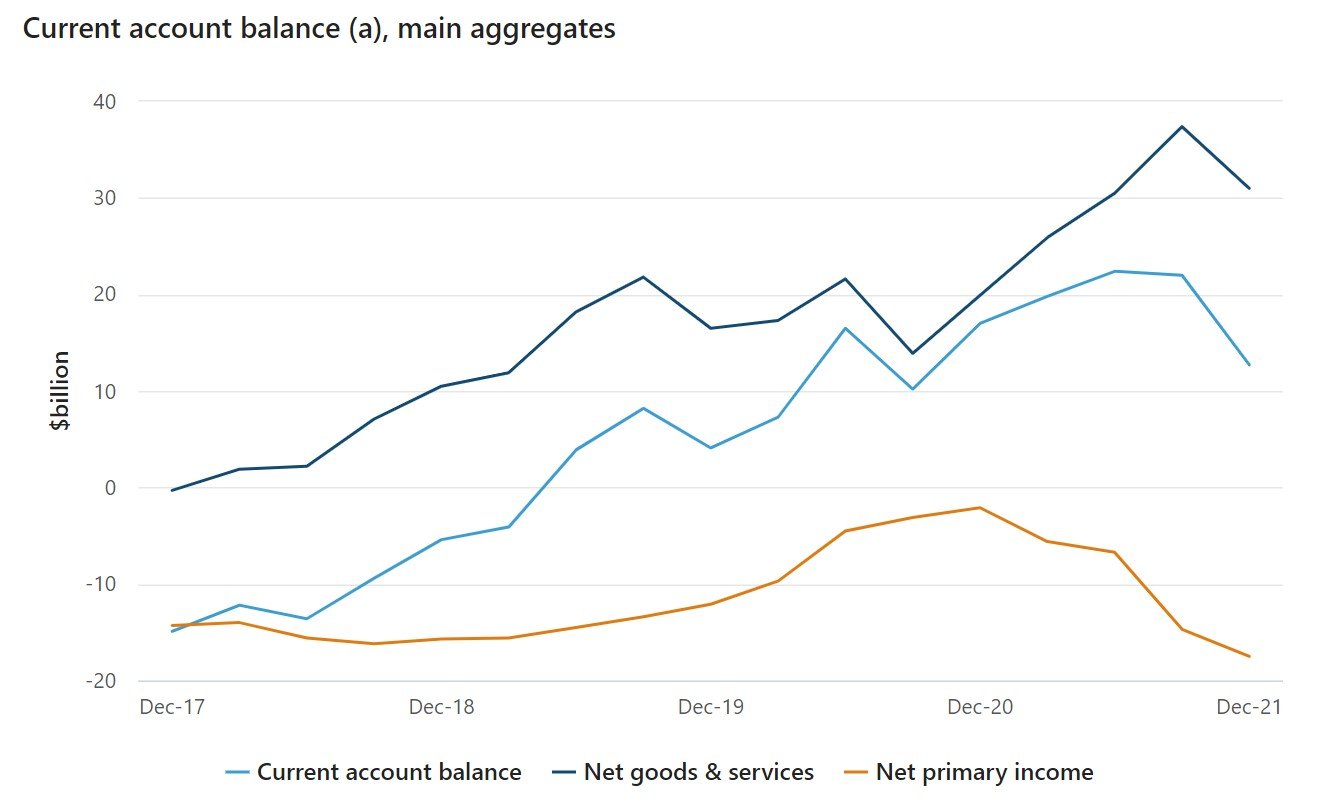

Have a look at this graph.

Source: Australian Bureau of Statistics

You can see that BoGS – the dark blue line – is leading the CA balance higher into surplus.

NPY is actually getting larger – the deficit is growing. This is pushing the CA balance the other way — so reducing the size of the surplus.

So the driver of the current CA surplus is the BoGS surplus. You can also call BoGS the trade balance or net exports.

Australia’s BoGS surplus is caused by an increase in Australia’s export sales (particularly of natural resources) and a slowdown in import spending (due to the impact of the pandemic).

What are the consequences of Australia’s CAS?

Here are some of the consequences of Australia’s CAS.

As Australia is selling more exports, there is greater demand for labour/resources into the export sector. This is to meet the growing demand for overseas markets.

Australia may also require greater investment in the mining sector to help increase the volume of natural resources that can be obtained and sold overseas. This could increase capital inflows in the form of loans from overseas. This, in turn, will increase income outflows and then increase the value of the NPY deficit.

In addition, as exports will be growing, they will contribute more to Australia’s aggregate demand. This is because AD = C+I+G+(X-M). So, as exports volumes rise, they will positively influence net exports (X-M), which will add positively to AD and the nation’s economic growth.

Not a lot of people are talking about the CAS. But they should be. It’s a very important statistic with important consequences for the Australian economy.

Want more on why Australia has a current account surplus?

I also have this video that looks at the drivers of a CAS (see below). It could be very helpful in trying to grasp this potentially tricky concept. A concept I never thought I’d see in my life.

Is a current account surplus a good thing?

Let’s start with my point: the current account balance is neither ‘good’ nor’ bad’.

(Okay, I’ll clarify. The current account deficit can be considered too large, if it hits around 6 plus per cent of GDP.)

But, in general, the government doesn’t label the current account balance as ‘good’ or ‘bad’. The Australian government doesn’t try to achieve a particular current account balance. You won’t see ScoMo on the news talking about how only his government can achieve a current account surplus (CAS).

This is because the government has limited control over the factors that drive the current account balance. The government can’t change the amount of exports or imports companies and people buy (trade balance). The government can control how much it borrows from overseas, but it cannot control how much private companies borrow from overseas (this affects the size of capital inflows and then the net primary income balance as a result).

I recently had some students comment on my YouTube channel about the advantages and disadvantages of a current account surplus. I wouldn’t think of it as having specific pros and cons.

I also wouldn’t talk about the government “should” reduce the current account deficit (CAD) or “should” achieve a CAS.

Instead, I would focus on the consequences of the current account balance. It’s a different perspective.

I would divide my thinking up between the consequences of a current account surplus (CAS) and deficit (CAD). If you’re writing about this in 2021, the focus is on the CAS.

Consequences of a CAS

In Australia we’re now talking about current account surpluses. What are the consequences of this?

Let’s think about this from the trade balance and then net primary income (NPY). This is because net exports and NPY are the key drivers of Australia’s current account balance.

Trade balance

If the trade balance is improving, Australia is selling more exports which is increasing GDP and the government’s revenue. This revenue can then be used on a range of functions across society to improve people’s standard of living.

If the trade balance is improving, Australians may be purchasing fewer imports. This could lead to greater purchases of domestically produced goods (maybe) which could boost GDP. The issue I have with this: Australia doesn’t produce the same goods as we import.

NPY

If NPY is shrinking, Australia has a greater stock of domestic funds (as these funds are not needed to service foreign debt). This could boost domestic savings and allow more projects to be funded domestically WITHOUT the need for foreign borrowing. Essentially Australia could shrink its savings-investment gap.

Consequences of a CAD

Your textbook will have a whole list of these. You can also see my video for help.

One thing to note: in the past, the world hasn’t seemed too concerned about the level of our CAD. As recently as 2015, Australia’s CAD was around 5.4 per cent of GDP. This did not spark a mass selling off of the $A!

In terms of positive consequences of a CAD? We could think about points such as:

If the trade balance worsens, maybe Australians have greater access to imports and this improves their standard of living

If the trade balance worsens, maybe Australian businesses have had a greater opportunity to purchase capital equipment for their operations and this could boost productivity and output for the economy

If the net primary income deficit increases, this means Australian individuals and businesses have been able to borrow more funds which could be used for productive purposes across the economy.

Another eco YouTuber (for your consideration)

I’ve discovered — or YouTube directed me to — another Eco teacher on YouTube.

He makes really great content — succinct and clear, easy to understand. No fluff.

You can find him here.

Here’s a great vid on the basics of the Balance of Payments.

Get clear on direct vs portfolio investment

Let’s turn to the Balance of Payments (BoP). This is the record of transactions (money coming into Australia; funds leaving Australia) between Australia and the rest of the world.

The BoP is divided into two accounts: the Current Account and the Capital and Financial Account (KAFA). We’ll focus on the KAFA.

(Why is the abbreviation for the Capital and Financial Account KAFA? Because the symbol for capital is ‘K’. Not ‘C’. C is for consumption).

The KAFA itself is divided into the Capital Account (the KA part) and the Financial Account (the FA part).

So many abbreviations.

Anyway, let’s stay with the FA part of the KAFA.

The FA has five main components:

Direct investment

Portfolio investment

Financial derivatives

Reserve assets

Other investment.

For this post, we’ll focus on direct and portfolio investment.

“The key here is the 10 per cent figure. Less than 10 per cent — think portfolio investment. Above 10 per cent — think direct investment.”

Portfolio investment

Think about an investment portfolio. This typically involves an individual holding a mix of investments, all of which are relatively small. The same logic applies here.

Portfolio investment involves an individual or a firm buying shares in an existing business. The size of this investment is less than 10 per cent of existing shares in the company.

An example? An American investor purchases A$1,000 worth of Telstra shares. The value (market capitalisation) of Telstra is A$42 billion as of November 2019. Clearly, this small investment is much less than 10 per cent of the value of the business!

Direct investment

This is all about creating totally new investment or buying more than 10 per cent of shares in an existing company.

So, we might see an Australian company buy more than 10 per cent of shares in an American company (this is also sometimes referred to as the Australian company taking a controlling stake in the US business). We could also see a foreign company start a subsidiary business in Australia (an Australian offshoot of its foreign operations; essentially the creation of a new business in Australia).

The key here is the 10 per cent figure. Less than 10 per cent — think portfolio investment. Above 10 per cent — think direct investment.

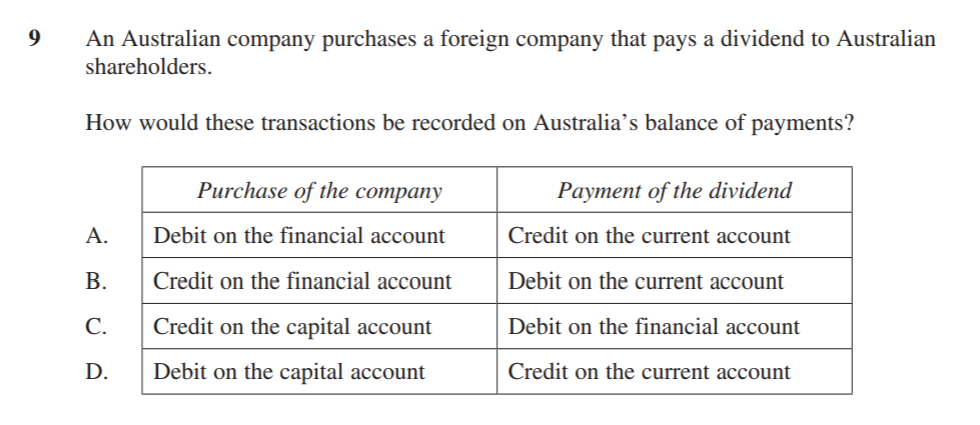

A potentially tricky BoP question

The 2018 NSW Economics HSC exam was full of challenging multiple choice questions. Here’s one that involves the Balance of Payments (BoP).

Check out the question below:

Source: NESA, 2018 Economics HSC

Let’s consider what we’ve got. From the question we know that we need to focus on Australia’s BoP, not the foreign country (whoever it is).

First bit of info: an Australian company purchases a foreign company.

This involves funds leaving Australia. And because it involves the purchase of a foreign company, this is likely to be a large amount of money. And and because it involves the purchase of a whole company, it is going to be classified as foreign direct investment (FDI).

FDI is recorded on the financial account. Therefore, this first bit of info would be recorded as a debit on the financial account.

Second bit of info: this foreign company then pays dividends to Australian shareholders.

Dividends are classified as an income flow. This means they are recorded on the current account, under primary income. If the dividends are paid to Australian shareholders, this represents an inflow (or credit) to Australia’s current account.

Then, this second bit of info would be recorded as a credit on the current account.

Our answer is A.

My working out process. See suggestions below.

My recommendation

Exams can be tricky situations. It can be easy to get the answer categories mixed up. I’d suggest working through the question first, putting your thinking down on paper, and THEN looking at the answer categories.

This way, you’ll know what you’re looking for and might be less likely to get tricked.

First time in my lifetime: a current account surplus

June 1975. Australia records a current account surplus.

September 2019. Australia records its next current account surplus.

This is an interesting development for the Australian economy. But, before we look at why this matters, let’s discuss what this all means.

Current account: the economic theory

Australia’s current account is part of the Balance of Payments (BoP). The BoP records transactions between Australia and the rest of the world. It’s a major measure of the nation’s external stability — Australia’s ability to successfully meet its foreign liabilities.

The BoP consists of the current account and the capital and financial account (KAFA). We’re just focussing on the current account here.

The current account shows inflows and outflows into Australia for trade in goods and services, income flows and other elements (such as transfer payments). Transactions on the current account are non-reversible.

Australia’s long history of current account deficits (CADs)

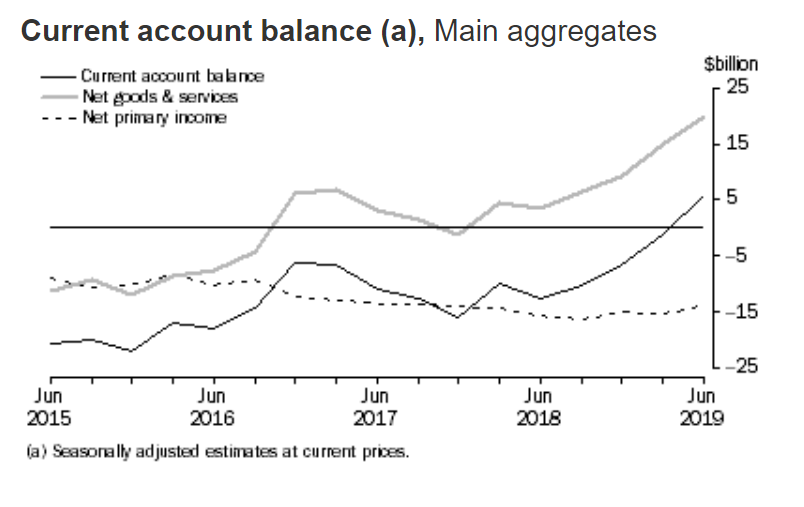

Between 1975 and 2019, Australia has recorded persistent CADs. This means outflows exceed inflows on the current account. In the graph below you can see the size of the CAD (as a percentage of GDP) between 2000 and 2019 in Australia.

The main causes (or main drivers) of a CAD involve the Balance on Goods and Services (net exports, or BoGS) and Net Primary Income (NPY). BoGS involves payments receipts for exports and imports of goods and services. NPY involves income flows, in and out of Australia, including dividends, rent and interest.

If you look at the graph below from the Australian Bureau of Statistics (ABS) you can see that NPY is usually in deficit. (We’ll go through why in another post.) But BoGS (net goods in the graph below) can fluctuate substantially and swing from deficit to surplus.

Source: ABS. Click the graph to go to the original source.

As of September 2019, BoGS is in surplus to the tune of $20 billion — the largest surplus recorded in Australia’s history. As a result, in September, the current account is now in surplus (a small surplus, $5 billion, but still a surplus).

Why does Australia (currently) have a current account surplus?

The current account surplus is due to the BoGS surplus. But don’t take my word for it. Here’s what ABS Chief Economist Bruce Hockman said.

"Six consecutive quarters of goods and services surpluses, broadly commodity driven, have laid the foundation for our first current account surplus in 44 years,” he said.

Mr Hockman added the export prices AND volumes had risen...while import volumes fell during the same period (potentially due to the depreciating Australian dollar making imports more expensive).

"Export volumes for the key bulk commodities of liquid natural gas, coal and iron ore were up, while volumes fell across several import categories resulting in an increased June quarter trade surplus," he said.

We’ll just have to wait and see if the current remains in surplus or whether this was a temporary event.

GOOD TO KNOW

BoGs is also known as the trade balance. So a BoGS surplus is also known as a trade surplus.

Test students on the Balance of Payments categories

Here’s a useful question from the 2017 NSW Economics HSC exam about the Balance of Payments.

I think this is a great revision exercise after you’ve looked at the BoP categories in a bit of detail. Click through for the whole exam paper. I don’t love the suggested answers, so I reckon you’re best served by developing some ideas yourself.

I’ve also done a walkthrough on this question (see below). This could help students see some useful ways to approach this question.